You're reading for free via Tunji Onigbanjo's Friend Link. Become a member to access the best of Medium.

Member-only story

5 Quick Points to Simplify the Federal Housing Administration Loan

One of the most important loan products to understand

A Federal Housing Administration (FHA) loan is a type of mortgage insured by the FHA and is issued by an FHA-approved lender. It can be used on residential properties ranging from single-family homes to four-plexes. FHA loans typically have 15-year or 30-year terms.

The FHA was established in 1934 by Congress through the National Housing Act of 1934. It was during the Great Depression when the housing industry was in extreme trouble. Back then, approximately 40% of households owned their homes. With the FHA being one of the leading programs for homeownership, as of Q2 2020, homeownership in the United States is at approximately 68%.

The FHA loan is known for primarily offering one of the lowest down payments if you meet the requirements at 3.5%. That means you can borrow up to 96.5% of that home you want. With that being said, the five following points need to be further understood to determine if the FHA loan is the right kind of mortgage product for you:

1. FHA Loan Requirements

2. Mortgage Insurance

3. Types of FHA Loans

4. FHA Loan Limits

5. Closing Costs

1. FHA Loan Requirements

When it comes to qualifying for a down payment as low as 3.5% for an FHA loan, the following are the requirements: a FICO score of at least 580, debt-to-income ratio less than 43%, the home must be your primary residence, you must have a steady income and proof of employment, and mortgage insurance.

When it comes to the FICO score requirement, a FICO score of at least 580 is the most important factor to qualify for a down payment as low as 3.5%. If your FICO score falls in the range of 500 to 579, you can still qualify for an FHA loan. Your down payment will instead be 10%. Down payments for FHA loans can come from savings, gifts, or a grant from a down payment assistance program.

Debt-to-income ratio is the percentage of your monthly gross income, income before taxes, that goes to paying monthly debts such as rent, mortgages, and credit cards. The simple formula is monthly expenses divided by monthly pre-tax income. Essentially, when it comes to qualifying for an FHA loan, your debt-to-income ratio should be less than 43%, meaning your monthly debt payments should only make up 43% of your gross monthly income.

For an FHA loan, you should have a steady income and proof of employment. What does that mean? You should have a record of steady income for the past two years at least. Additionally, you should have proof of your current employment. If you are self-employed, you will need two years of successful self-employed history showing your income. If you have been self-employed for less than two years but more than one year, you may be eligible for an FHA loan still if you can provide income and employment history for two years before becoming self-employed.

Mortgage insurance, which will be covered in the next session, is another important requirement. Before moving on, it is important to state that you should have a social security number, reside in the United States lawfully, and be of legal age (based on your state) to sign a mortgage.

2. Mortgage Insurance

Mortgage Insurance is a required part of FHA loans. There are two parts to mortgage insurance: an upfront mortgage insurance premium (MIP) and an annual MIP. The upfront MIP is typically equal to 1.75% of the base value of the loan. Upfront MIP can be paid at the time of closing on a home, or it can be rolled into your FHA loan.

Annual MIP, which is typically paid monthly, ranges from 0.45% to 1.05% of the base value of the loan. Annual MIP values may differ depending on the loan amount, the loan’s length, and the loan-to-value ratio. For a quick breakdown, loan-to-value ratio is the value of the mortgage divided by the appraised value of the property value, which can be seen as the loan amount divided by the current total market value of the property. Annual MIP payments can occur for either 11 years or the loan’s life, depending on the length of the loan and the loan-to-value ratio.

3. Types of FHA Loans

The following are the different common types of FHA loans: Fixed Rate Mortgage, Adjustable-Rate Mortgage, 203(k) Mortgage, Energy Efficient Mortgage, Section 245(a) Loan, and Home Equity Conversion Mortgage.

A Fixed Rate Mortgage is a mortgage where the interest rate remains the same through the term of the loan and full amortizes. Since the interest rate remains constate, monthly payments do not change.

An Adjustable-Rate Mortgage is when the loan’s initial interest rate is lower for a certain amount of time. After the introductory interest rate period, monthly payments will increase, or in some cases decrease, according to the interest rate, which is tied to an adjustment index.

A 203(k) Mortgage factors in the cost of certain repairs and renovations into the loan. That means that you can borrow money for both the purchase of the home and improvements, which can make a big difference if you do not have much cash on hand immediately.

An Energy Efficient Mortgage is a similar concept to the 203(k) Mortgage, but instead it is aimed at upgrades that can lower your utility bills. The idea behind it is that energy-efficient homes have lower operating costs, which lowers your bills over time and frees up your income for mortgage payments or other expenses.

A Section 245(a) Loan is for borrowers who expect their income to increase over time. The two kinds of mortgages that fall under it are the Graduated Payment Mortgage and the Growing-Equity Mortgage. A Graduated Payment Mortgage starts with lower initial monthly payments that gradually increase over time. A Growing-Equity Mortgage has scheduled increases in monthly principal payments that result in shorter loan terms.

A Home Equity Conversion Mortgage is a reverse mortgage that helps seniors aged 62 and older convert the equity in their homes to cash while retaining the title to their home. A senior can choose to withdraw the funds either as a fixed monthly amount or as a line of credit.

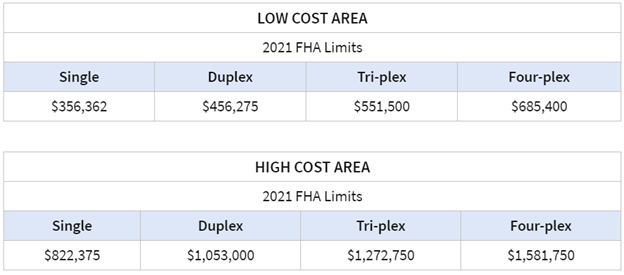

4. FHA Loan Limits

FHA loan limits are important to understand. Loan limits will vary by the kind of area you are purchasing a property in and the number of units in the property. The following breakdown by FHA.com showcases FHA loan limits for 2021:

5. Closing Costs

Closing costs are always important to know about no matter what mortgage or loan product you are signing up for. Closing costs include items such as lender’s origination fee, deposit verification fees, attorney fees, appraisal fees, inspection fees, cost of title insurance, document preparation, property survey, credit reports, certification fees, recording fees, tax service fees, and home inspection fees.

When it comes to FHA loans, the average closing costs range from 2% to 4% of the loan amount. It is important to note that your closing costs are separate from your down payment. Some FHA-approved lenders will combine closing costs and your down payment and call it something such as “cash due at closing.”

FHA loans sound great, but it comes down to you doing your research and due diligence to determine if it is truly the right mortgage product for you. Maybe a conventional mortgage, USDA loan, or VA loan may be a better option. Purchasing a home will be a major point in your life. Truly understanding what route will be the best for you will save you money in the long-run and allow you to continue down the road of long-term financial success.